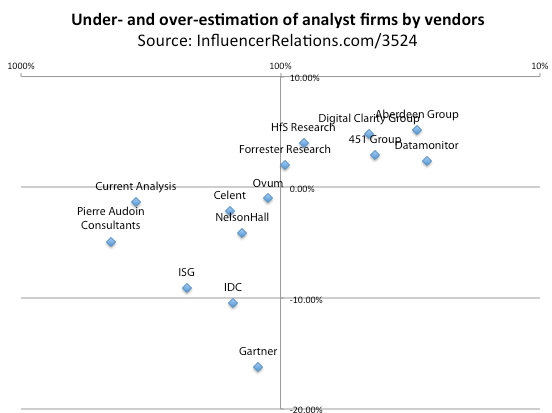

2014 has been the breakout year for freemium analyst firms. It’s fundamentally ended the fantasy that only Gartner and Forrester were “deal-maker or breaker” firms. An excellent illustration of that is the chart below, which uses data from the Analyst Value Survey. It shows the firms where the demand-side and supply-side respondents gave the most different answers to the question: which firms most influence buyers.

Here’s how to understand the chart, first in terms of meaning, and second in term of method:

- Meaning. In the opinion of people on the demand-side, firms like Aberdeen and DCG have substantially more influence on buyers than the supply-side admits, and Gartner and IDC have substantially less influence on buyers than the supply-side thinks.

- Method. Firms that are higher up were more often said to be more influential on buyers by people on the demand-side than buy people on the supply side (it’s the absolute gap between the scores given by those two groups, not the absolute scores). The horizontal axis shows the ratio between those numbers, and you can ignore that for now. If you want the run the numbers yourself, you can buy the AVS here.

Gartner and Forrester are, as always, the firms that are said to be most influential. But there’s a difference between the demand- and supply-side in how strongly they see that leadership. Some firms are substantially under-estimated by the supply-side: Aberdeen, DCG, HfS, 451, Datamonitor and Forrester. Suppliers are not putting enough effort into those overlooked firms.

One example: 30% of supply-side people say IDC influences buyers, but only 20% on the demand side. Over 21% of people on the demand side say HfS Research influence buyers, but only 17% on the supply side. So, if most firms put twice as much AR effort into IDC than into HfS, but HfS is actually more influential then that is lost opportunity.

As Chevkov might have said, all overlooked analyst firms are different: Aberdeen is not an analyst in our opinion, but a research firm delivering content services. DCG and HfS are freemium firms. 451 and Datamonitor have weak business development aimed at vendors (and vendors can’t address themselves to Datamonitor’s tech-agnostic expertise in energy, healthcare, finance and consumer goods).

These lost opportunities are not occurring for simple reasons. Nor are they easy to turn around: Aberdeen, for example, is hardly open to non-client influence. But they reflect a real perception gap, and some wasted effort that needs to be shifted.

Of course this picture will be different for each industry: services is the major part of the industry now, but services analyst firms might not be influential in an equipment segment.

This post originally appeared on InfluencerRelations.com.

Ready for more? Subscribe to Kea Company’s Influencer Insights

Join hundreds of peers and get Kea Company’s latest blogs, webinars and downloadable content straight to your inbox. Enter your email address below:

Error: Contact form not found.

[…] the supply side. It seems that these two top firms have rather different value propositions. As we noted last month, Gartner is more highly rated by the supply-side than by the […]

[…] customers, naturally producing less revenue and fewer users than its vendor clients. In contrast, DCG’s freemium model gives it both a wider audience and paid engagements that are deeper than Constellation’s […]

[…] 31% of the total is held by Gartner. While that confirms Gartner’s leadership, it also dispells the myth that Gartner alone holds most of the analyst community’s influence on purchasing. That influence […]